Withholding tax on Bangkok creator invoices in 2026

By Mai Influence

A Bangkok creator quotes 40,000 THB. You wire 38,800 and the creator sends you a passive-aggressive Line message. Or you wire the full 40,000 and your finance lead flags it three weeks later because nothing got filed with the Revenue Department. Both versions happen every week to SEA brand marketers who have never had to run a Thai withholding tax line before, and both cost more to fix than to plan.

This is the piece nobody wants to write because it is boring, and the piece every finance team asks about the minute the first Bangkok invoice lands. We run it here so a marketer in Singapore or KL can walk into their next brief already knowing which rate applies, which form gets filed, and which clause needs to be in the payment terms section of the contract before the shoot day.

What Thai law actually asks you to withhold

If your company is registered in Thailand and you pay a Thai creator for a service, you are the payer of record. The Revenue Code makes you deduct a slice of the invoice at source, remit it to the Revenue Department by the 7th of the following month, and hand the creator a withholding tax certificate that they use to reconcile their own annual return.

For most creator work in 2026, the rate lands in one of two places. Straight service fees to an individual or a juristic person come in at 3%. Work that is billed as an advertising service to a juristic person can drop to 2%, which is why so many Bangkok agencies bill under "advertising service" line items even when the shoot is a single Reel. The safe default when you are not sure is 3%. The 1% saving is real over a year of retainer work but not worth misclassifying a brief that is really content production dressed up as an ad buy.

If the creator invoices as an individual, you file PND-3. If they invoice through a registered company or a partnership, you file PND-53. Same 7th-of-the-month deadline, different form, different penalty regime if you miss it. The penalty is not catastrophic on one late filing, but it compounds quickly across a roster of ten creators paid monthly.

The gross-up trap SEA brands keep paying twice

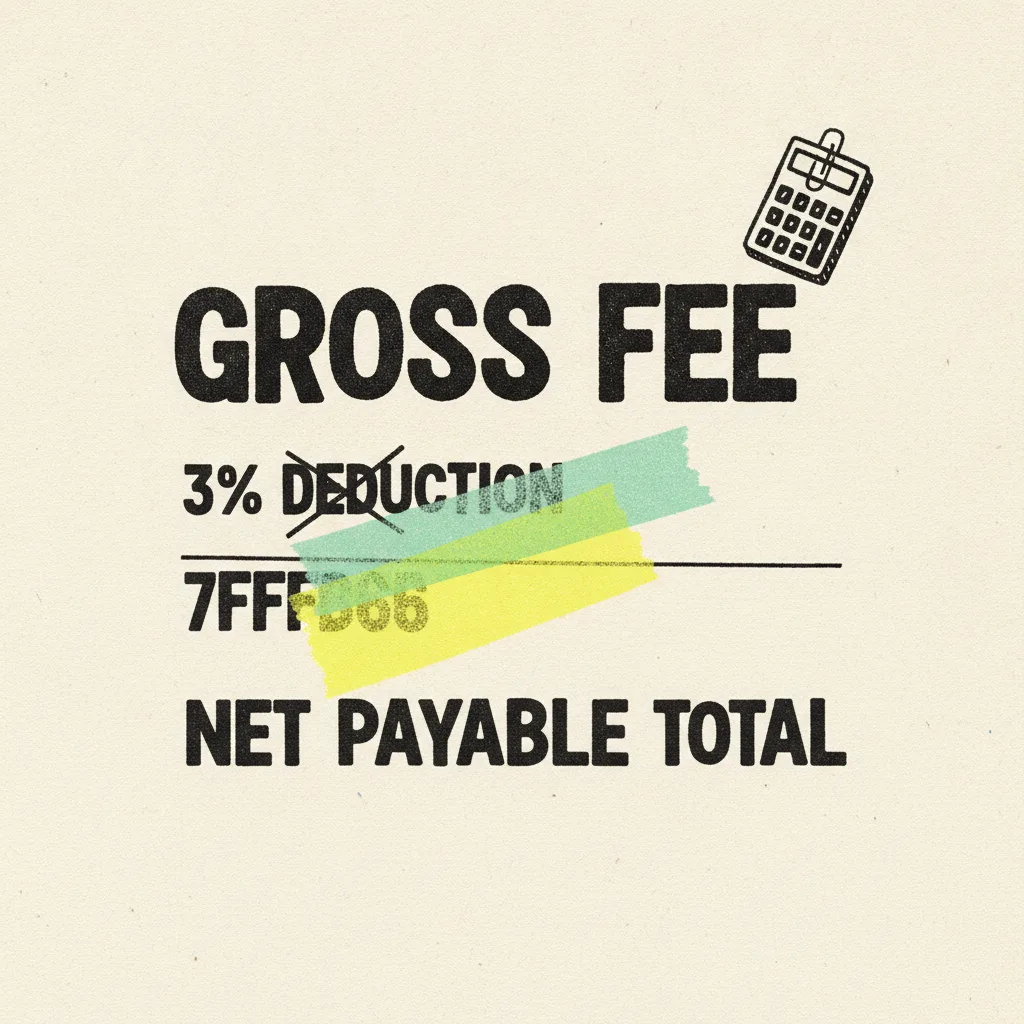

Here is the failure mode we see on almost every first-time cross-border brief. The creator's rate card says 40,000 THB for a Reel. The brand marketer approves 40,000. Finance withholds 3% and wires 38,800. The creator raises the invoice again asking for the 1,200 back because their agent quoted the take-home number. Now the brand is arguing about 1,200 THB with someone who is holding the deliverable hostage.

There are only two clean ways to handle this, and you pick one before the contract is signed:

- Net-of-tax quote. The 40,000 is what the creator receives after withholding. The gross-up on your side is 40,000 divided by 0.97, which lands at 41,237 THB. You wire 40,000, remit 1,237 to the Revenue Department, hand the creator a certificate for the deducted amount.

- Gross quote with withholding disclosed. The 40,000 is the invoice face value. You wire 38,800, remit 1,200 to the Revenue Department, hand over the certificate. The creator gets 38,800 in the bank and 1,200 back as tax credit on their annual return.

Neither is wrong. What is wrong is not deciding until the wire is queued. Write the words "of which Thai withholding tax will be deducted at source" or "net of Thai withholding tax" into the brief template before you ever send it, and the argument stops happening.

What changes when the payer is not in Thailand

Cross-border briefs from Singapore, Malaysia, or Indonesia get a different tax picture, which we walked through in more detail in the SG and MY cross-border piece. Short version: if the paying entity has no Thai tax presence, you generally cannot withhold in Thailand at all, and the creator is fully responsible for declaring the income on their own return. That does not mean the brief is tax-free. It means the tax burden has quietly shifted to the creator, and any experienced Bangkok creator will factor that into the quote.

The trap is a Singapore brand assuming Thai withholding still applies and shaving 3% off the wire anyway. That is not a legal withholding, it is just a short payment, and the creator has grounds to hold the deliverable until it lands.

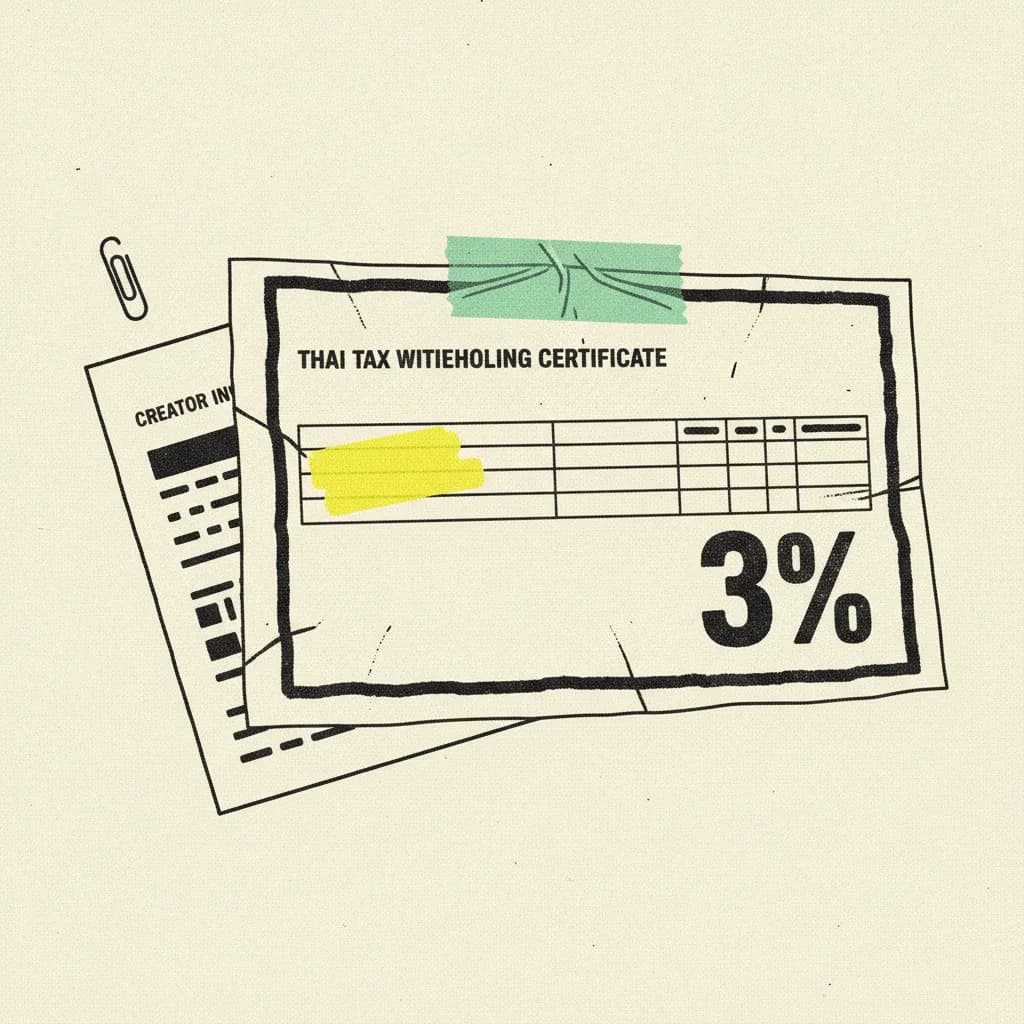

What actually goes on the withholding certificate

The withholding tax certificate you hand the creator is the piece of paper that makes the deduction legal from their side. It has to name the payer's tax ID, the creator's tax ID or ID card number, the gross amount, the rate applied, the deducted amount, and the payment date. Bangkok creators who have done this before will ask for it in soft copy within a week of payment. Creators newer to brand work will not ask, and then discover in March that they cannot claim the credit without it.

The certificate is not a courtesy. It is what turns your withholding from a short payment into a tax credit the creator can use.

The clauses to write into every Bangkok brief

Four lines in the contract handle 90% of the friction. Add them once, use them everywhere.

- Rate basis. "The fee stated above is [gross of / net of] Thai withholding tax."

- Applicable rate. "Payer will withhold at [3% / 2%] under section [3 ter / 3 tredecim] of the Revenue Code."

- Certificate delivery. "Payer will issue the withholding tax certificate to the payee within 14 days of payment."

- Invoice format. "Invoice must include payee tax ID or ID card number and registered address."

That last line is the one brands forget until finance sends the invoice back. Bangkok creators working through a manager will have this on their rate card already. Nano and micro creators booking directly will not, and you will chase it during the same week the post is meant to go live. Ask for it at brief stage, not payment stage, and the timeline holds.

We hold the escrow on Mai Influence so the tax mechanics run before the payment reaches the creator, not after. The 3% comes off the top, the certificate is generated automatically, and the brief moves. It is not the reason brands sign up, but it is the reason finance stops flagging the Bangkok line on the media plan.